We’re supportive of JIP-33. Objectively the immediate economics favor Coinbase, with commissions of 5%/10% + redirected management fees mean the DAO foregoes ~$210K annually if TVL potentially grows 16% in our base case assumption. But more importantly, we see this as Jito signaling unwavering commitment to BAM adoption, even if that means sacrificing some revenue in the short-term.

Coinbase brings 8.99M SOL in current addressable stake and retail distribution that has not yet been accessible for JitoSOL. The lending product unlocks $230M+ in borrowing capacity using our base case assumption, and also enables looping leverage that could amplify TVL growth by 1.5x - 1.7x, further enhancing the stake weight of BAM Jito can achieve via Coinbase.

Economics

The ordinary 4% management fee flows to Coinbase, not the DAO. In our base case, DAO revenue drops from $4.41M to $4.20M assuming 16% TVL growth. In this case Coinbase captures $650K. This is the cost of the partnership, and we think it’s worth paying.

| Scenario | TVL | DAO Revenue | Coinbase Capture |

|---|---|---|---|

| Current | 14.43M | $4.41M | N/A |

| Bear (+6%) | 15.33M | $4.33M | $273K |

| Base (+16%) | 16.67M | $4.20M | $650K |

| Bull (+31%) | 18.92M | $4.04M | $1.26M |

Addressable Market

Coinbase runs 8.99M SOL across four validators, representing 62% of current JitoSOL TVL. Stake accounts could be transferred for existing users, as well as receive net new stake.

Growth

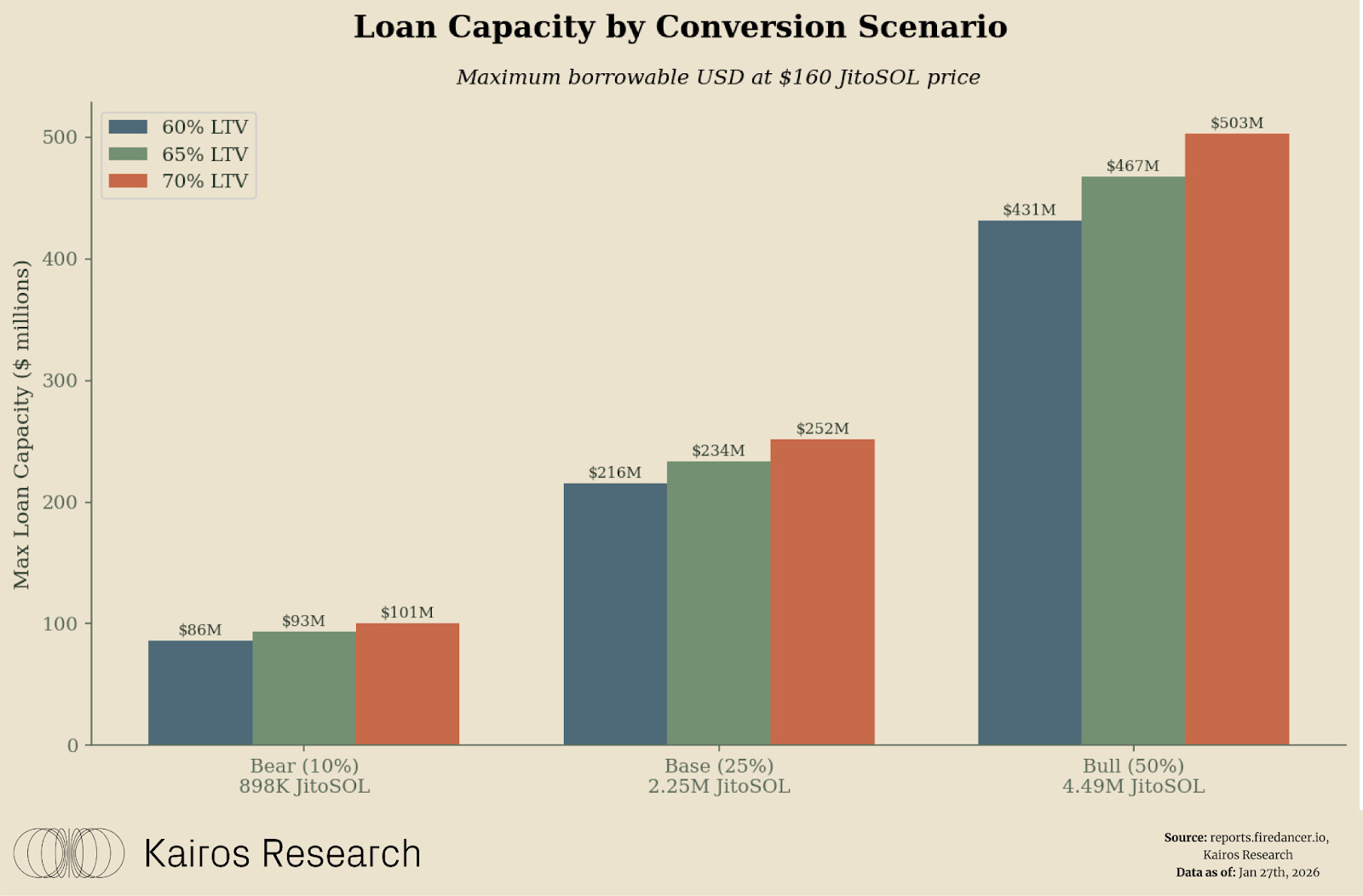

The conversion rates in our model (10%, 25%, 50%) refer to what percentage of Coinbase’s 8.99M SOL converts to JitoSOL. The TVL growth percentages (6%, 16%, 31%) are the resulting impact on JitoSOL’s 14.43M TVL.

So the mapping is as follows:

Bear: 10% conversion × 8.99M = 0.9M new SOL → +6.2% TVL growth

Base: 25% conversion × 8.99M = 2.25M new SOL → +15.6% TVL growth

Bull: 50% conversion × 8.99M = 4.49M new SOL → +31.1% TVL growth

Looping Leverage: The Multiplier Effect

The interesting aspect about the partnership in our opinion is that the lending product doesn’t just create borrowing capacity it enables recursive leverage that amplifies key metrics.

The mechanics: A user deposits JitoSOL → borrows USD at 65% (this is a hypothetical LTV) LTV → buys SOL → mints more JitoSOL → repeats. At 65% LTV with 4 loops, 1M JitoSOL becomes 2.53M of exposure. The theoretical max is 2.86x (1/(1-0.65)), but practically we model 2-2.5x for active loopers.

Why this matters for BAM:

-

TVL Expansion: If 50% of new Coinbase users loop, the 2.25M base case becomes 3.4M effective TVL (+51% vs no looping)

-

Coinbase Pool Share: Looping amplifies Coinbase’s share of the JitoSOL pool from 13.5% to 19%+ depending on participation

-

BAM Stake Weight: More JitoSOL = more stake routed through Jito’s validator set. At 50% looping, CB’s share of network stake grows from 4.2% to 4.5%

This is the unintentional potential flywheel Jito could have: lending utility → looping demand → TVL growth → larger stake weight → more MEV capture → better yields → more adoption.

| Looping Participation | Effective New TVL | Coinbase Pool Share | Coinbase Network |

|---|---|---|---|

| No Looping | 2.25M | 13.50% | 4.20% |

| 30% Loop | 2.9M | 16.90% | 4.30% |

| 50% Loop | 3.4M | 19.00% | 4.50% |

| 70% Loop | 3.8M | 21.00% | 4.60% |

Lending Capacity

At 65% LTV and base conversion: $234M capacity without looping. With moderate looping participation, effective capacity scales to $350M+. This creates sticky, utility-driven demand that compounds Coinbase’s contribution to the pool. For context, Coinbase offers ~86% LTV for cbBTC/USDC loans

Overall JIP-33 is further proof that Jito’s primary focus is BAM adoption. The economics subsidize Coinbase, but the lending product potentially creates a leverage flywheel that amplifies TVL, Coinbase’s pool share, and BAM’s network stake weight. Ultimately this prop is betting that distribution and utility compound faster than short-term yield dilution. We think this is the right long term bet.